Charting Bank-to-Platform Pathways for Protected Repeat Charges in American Digital Retail Networks

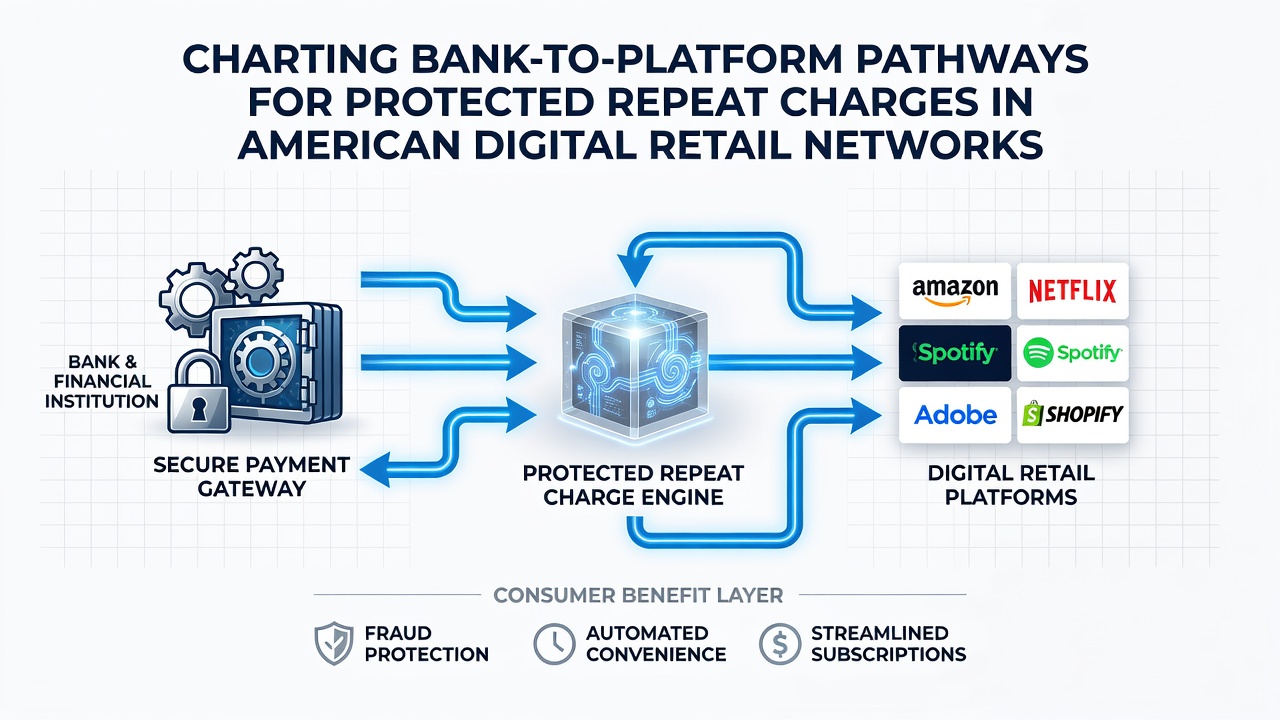

American digital retail networks rely on intricate connections between banks and online platforms to handle protected repeat charges, and these pathways have evolved through layers of verification, authorization, and settlement processes that keep transactions moving efficiently. Data from payment system operators shows that recurring billing now accounts for a substantial portion of e-commerce volume, with merchants depending on stable routes that link financial institutions directly to subscription management systems. Observers note that these routes incorporate multiple checkpoints designed to confirm account validity before any funds transfer occurs.

American digital retail networks rely on intricate connections between banks and online platforms to handle protected repeat charges, and these pathways have evolved through layers of verification, authorization, and settlement processes that keep transactions moving efficiently. Data from payment system operators shows that recurring billing now accounts for a substantial portion of e-commerce volume, with merchants depending on stable routes that link financial institutions directly to subscription management systems. Observers note that these routes incorporate multiple checkpoints designed to confirm account validity before any funds transfer occurs.Core Components of Bank-to-Platform Routing

Payment networks in the United States route repeat charges through established channels that include the Automated Clearing House operated by NACHA along with major card associations, and each channel maintains its own set of rules for authorization and settlement. Retail platforms integrate with these networks via APIs that transmit customer payment details while preserving encryption standards that prevent interception during transfer. Research indicates that successful routing depends on real-time communication between the merchant's system and the originating bank, where account status checks occur before the charge request advances further into the network.

Those who manage high-volume subscription services often discover that direct integration points reduce processing delays, since fewer intermediaries stand between the bank and the retail platform. Figures from industry reports reveal that platforms handling monthly billing cycles have adopted standardized messaging formats that allow banks to respond within seconds rather than hours. This setup supports protected operations because each step includes embedded identifiers that flag anomalies before settlement completes.

Verification Layers Along the Pathway

Verification begins at the bank level when a customer authorizes recurring access, and the platform then receives tokens or reference numbers that replace raw account data for subsequent charges. Experts have observed that this token exchange limits exposure while still permitting the bank to validate ownership during every billing cycle. In June 2026, updated guidelines from the Federal Reserve encouraged broader adoption of dynamic verification tokens across retail platforms, which has strengthened the connection points between banks and digital storefronts.

Additional safeguards appear in the form of velocity checks and pattern analysis that run in parallel with the main authorization flow, and these tools compare current requests against historical data stored at the network level. Retail operators report that combining bank-side validation with platform-side monitoring creates overlapping protection that catches discrepancies early in the process. The result shows up in lower reversal rates for repeat transactions across multiple retail categories.

Settlement and Reconciliation Mechanisms

Once authorization clears, funds move through settlement systems that reconcile debits and credits between the customer's bank and the merchant's acquiring institution, and this phase includes batch processing windows that align with daily cutoffs established by network operators. Platforms coordinate with banks to receive confirmation files that detail which charges succeeded and which require follow-up action. Studies from payment research centers indicate that automated reconciliation tools now handle the majority of these files, reducing manual review time for finance teams at retail companies.

Protected repeat charges benefit from these coordinated flows because any mismatch triggers immediate alerts that route back through the same pathways for correction. Observers note that settlement transparency helps merchants maintain accurate cash-flow projections while complying with network rules that govern timing and reporting. Retail networks continue to refine these mechanisms to accommodate growing transaction volumes without introducing additional friction for end customers.

Regulatory Influences on Pathway Design

Federal regulations shape how banks and platforms structure their connections, particularly rules that address consumer protections during recurring billing arrangements. Compliance requirements mandate clear disclosure of charge amounts and frequencies, which platforms must embed into the authorization process before any repeat transaction occurs. Data from regulatory filings shows that adherence to these standards has prompted many digital retailers to update their integration protocols with banks to include automated notification systems.

Industry associations have published frameworks that outline best practices for maintaining secure pathways, and these documents emphasize consistent logging of authorization events across the entire route from bank to platform. Retail participants who follow such frameworks report smoother audits because documentation flows naturally through the established channels. The regulatory environment continues to influence how new connection points are built, especially as volume grows in subscription-based retail models.

Conclusion

Bank-to-platform pathways for protected repeat charges form the backbone of American digital retail operations, and ongoing refinements in verification, settlement, and regulatory alignment keep these routes reliable. Platforms that map their connections carefully gain operational stability while meeting network expectations for security and accuracy. As transaction patterns shift, the infrastructure supporting these pathways adapts through incremental updates that preserve the core flow between financial institutions and retail systems.