How Retail Startups Sync Bank Feeds With Digital Checkout Flows to Handle Recurring Charges Without Extra Layers

Retail startups have developed methods to connect bank account data streams directly to their digital checkout systems, allowing recurring charges to process through automated bank feeds rather than relying on additional payment intermediaries. This approach uses API connections that pull verified account information at the point of purchase, then schedule deductions on a repeating basis using the same data pathway. The process begins when a customer enters banking details during checkout, at which point the system queries the bank feed in real time to confirm account status and ownership. Once validated, the platform stores a secure reference that triggers future charges without requiring the customer to re-enter information or pass through separate authorization steps. Data from industry reports shows that direct bank feed synchronization reduces the number of required handoffs between systems, which in turn lowers the points where transaction details could be exposed.

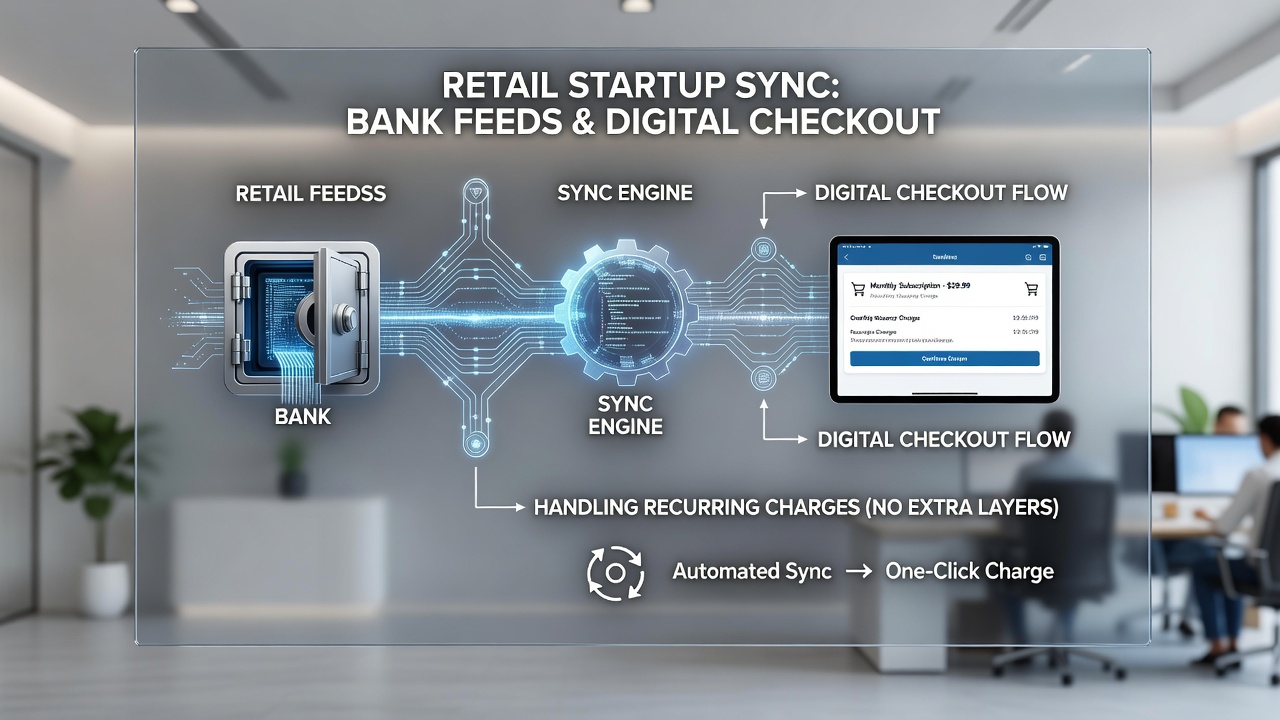

Retail startups have developed methods to connect bank account data streams directly to their digital checkout systems, allowing recurring charges to process through automated bank feeds rather than relying on additional payment intermediaries. This approach uses API connections that pull verified account information at the point of purchase, then schedule deductions on a repeating basis using the same data pathway. The process begins when a customer enters banking details during checkout, at which point the system queries the bank feed in real time to confirm account status and ownership. Once validated, the platform stores a secure reference that triggers future charges without requiring the customer to re-enter information or pass through separate authorization steps. Data from industry reports shows that direct bank feed synchronization reduces the number of required handoffs between systems, which in turn lowers the points where transaction details could be exposed.Core Components of the Synchronization

Bank feeds operate through standardized protocols that allow retail platforms to receive account verification signals and transaction confirmations in a continuous loop. These feeds link the checkout flow to the originating bank account, enabling the startup to initiate ACH debits or similar electronic transfers on scheduled dates. The checkout interface handles both the initial capture and the recurring trigger within a single data environment, eliminating the need for external schedulers or additional gateways. Observers note that retail startups often embed these connections using open banking standards that have expanded since the early 2020s. In practice, the system pulls balance and status updates from the bank at regular intervals, ensuring the recurring charge attempt only proceeds when sufficient funds exist. This built-in check occurs without separate verification services because the bank feed itself supplies the necessary indicators.Implementation in Recurring Billing Scenarios

Startups that manage subscription-style retail models, such as recurring product deliveries or membership services, configure their checkout to map each customer’s bank reference to a billing calendar. When the due date arrives, the platform sends a debit request through the same feed channel that handled the initial signup. The absence of extra layers means the transaction moves from the retail system straight to the bank network, with confirmation returned along the identical pathway. Figures from payment industry analyses indicate that this method supports higher volumes of micro-recurring charges because each transaction avoids cumulative fees associated with stacked processors. The direct link also allows immediate updates if a customer changes bank accounts, since the feed can detect and prompt re-verification within the existing checkout framework.