How Subscription Platforms Use Merchant Account Setups to Streamline Fraud Checks During Recurring Customer Billing

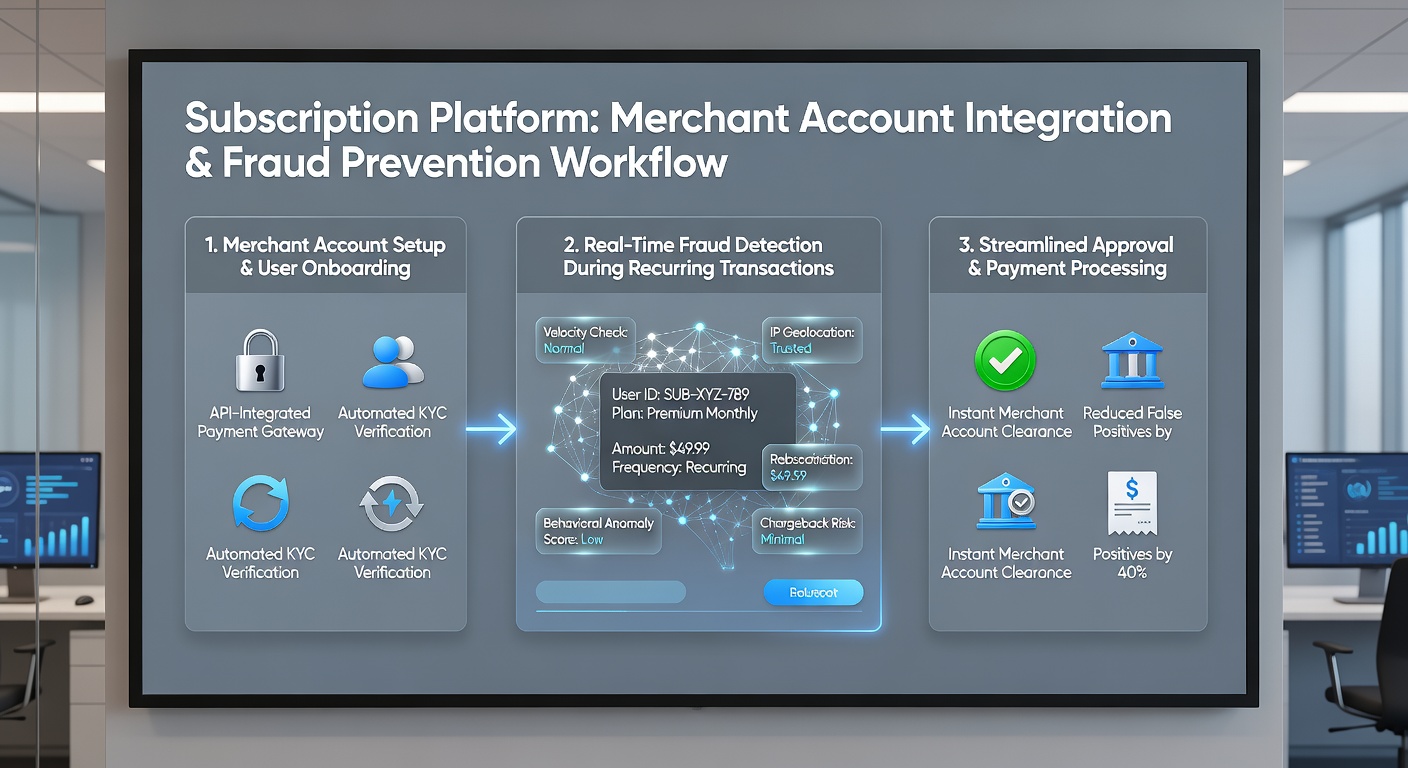

Subscription platforms rely on carefully configured merchant accounts to manage the unique demands of recurring customer billing while reducing exposure to fraudulent transactions. These setups allow businesses to process ongoing payments efficiently and incorporate automated verification steps that flag suspicious activity before charges clear. Research indicates that platforms handling subscriptions experience higher fraud risks during initial sign-ups and subsequent renewals because stolen card details often surface only after multiple billing cycles. Merchant account providers equip subscription services with tools that separate one-time purchases from recurring ones. This distinction matters because card networks apply different rules to standing authorizations. When a platform registers a subscription through its merchant account it can attach specific descriptors and risk parameters that trigger tailored fraud screening. Observers note that such configurations reduce false declines on legitimate renewals while catching anomalies like sudden geographic shifts or mismatched device data.

Subscription platforms rely on carefully configured merchant accounts to manage the unique demands of recurring customer billing while reducing exposure to fraudulent transactions. These setups allow businesses to process ongoing payments efficiently and incorporate automated verification steps that flag suspicious activity before charges clear. Research indicates that platforms handling subscriptions experience higher fraud risks during initial sign-ups and subsequent renewals because stolen card details often surface only after multiple billing cycles. Merchant account providers equip subscription services with tools that separate one-time purchases from recurring ones. This distinction matters because card networks apply different rules to standing authorizations. When a platform registers a subscription through its merchant account it can attach specific descriptors and risk parameters that trigger tailored fraud screening. Observers note that such configurations reduce false declines on legitimate renewals while catching anomalies like sudden geographic shifts or mismatched device data.Key Elements of Merchant Account Setup for Recurring Transactions

Platforms begin by selecting merchant account categories that support recurring billing indicators. These categories enable processors to recognize subscription patterns and apply velocity checks across multiple billing periods rather than isolated events. Data shows that accounts set up with proper recurring flags experience fewer chargebacks because issuers receive clearer signals about expected transaction frequency and amounts.

Integration with address verification systems and card verification value checks occurs at the account level. Subscription platforms often configure their merchant accounts to retain verified billing details for future cycles while requiring re-authentication only when risk scores rise. This approach maintains customer convenience without sacrificing security layers that banks demand for high-volume recurring flows.

Automated Fraud Screening During Billing Cycles

Once the merchant account activates recurring capabilities the platform can route each billing attempt through layered fraud filters. These filters examine historical transaction data tied to the specific customer profile stored under the account. When patterns deviate such as an unusual increase in failed attempts followed by a success the system can pause the charge and request additional verification.

Account updater services form another component many platforms activate within their merchant setups. These services automatically refresh expired card information with issuers which prevents legitimate subscription interruptions that might otherwise prompt customers to enter new details through unsecured channels. Figures reveal that platforms using updater features alongside fraud tools see measurable drops in account takeover attempts during renewal periods.

Regulatory Context and Compliance Adjustments in 2026

By May 2026 several payment networks had updated their guidelines for recurring transactions prompting merchant account providers to adjust risk parameters accordingly. Platforms responded by embedding stronger authentication triggers at the account setup stage particularly for cross-border subscriptions. According to reports from the Federal Reserve these adjustments helped align merchant configurations with evolving data security expectations without disrupting billing continuity.

Industry studies further highlight how merchant accounts configured for subscription services incorporate real-time monitoring dashboards. These dashboards aggregate chargeback ratios and dispute reasons across recurring cohorts allowing platforms to refine fraud rules dynamically. Researchers discovered that early adoption of such monitoring within merchant setups correlates with lower overall loss rates in subscription-heavy sectors.

Practical Implementation Across Different Business Models

Take one media streaming service that restructured its merchant account to flag high-risk geographies during recurring authorizations. The platform combined this with device fingerprinting data pulled at the initial signup so subsequent billings inherited a baseline risk score. Experts have observed that this method cuts manual review workloads significantly while preserving revenue from genuine international subscribers.

Another example involves software-as-a-service companies that layer their merchant accounts with automated retry logic. Instead of immediate declines on suspected fraud the setup schedules limited retries paired with customer notifications. This balances fraud prevention against the reality that temporary network issues sometimes mimic suspicious behavior during billing runs.

Conclusion

Subscription platforms achieve smoother fraud management when they design merchant account setups around the predictable nature of recurring billing. These configurations support specialized screening, account updating, and compliance alignment that standard merchant accounts often lack. As transaction volumes grow and regulatory expectations shift, the ability to embed fraud controls directly into the merchant account infrastructure continues to shape how platforms protect both revenue and customer trust.