Mapping the Connections Between Financial Service Providers and Digital Storefronts to Support Protected Charge Operations

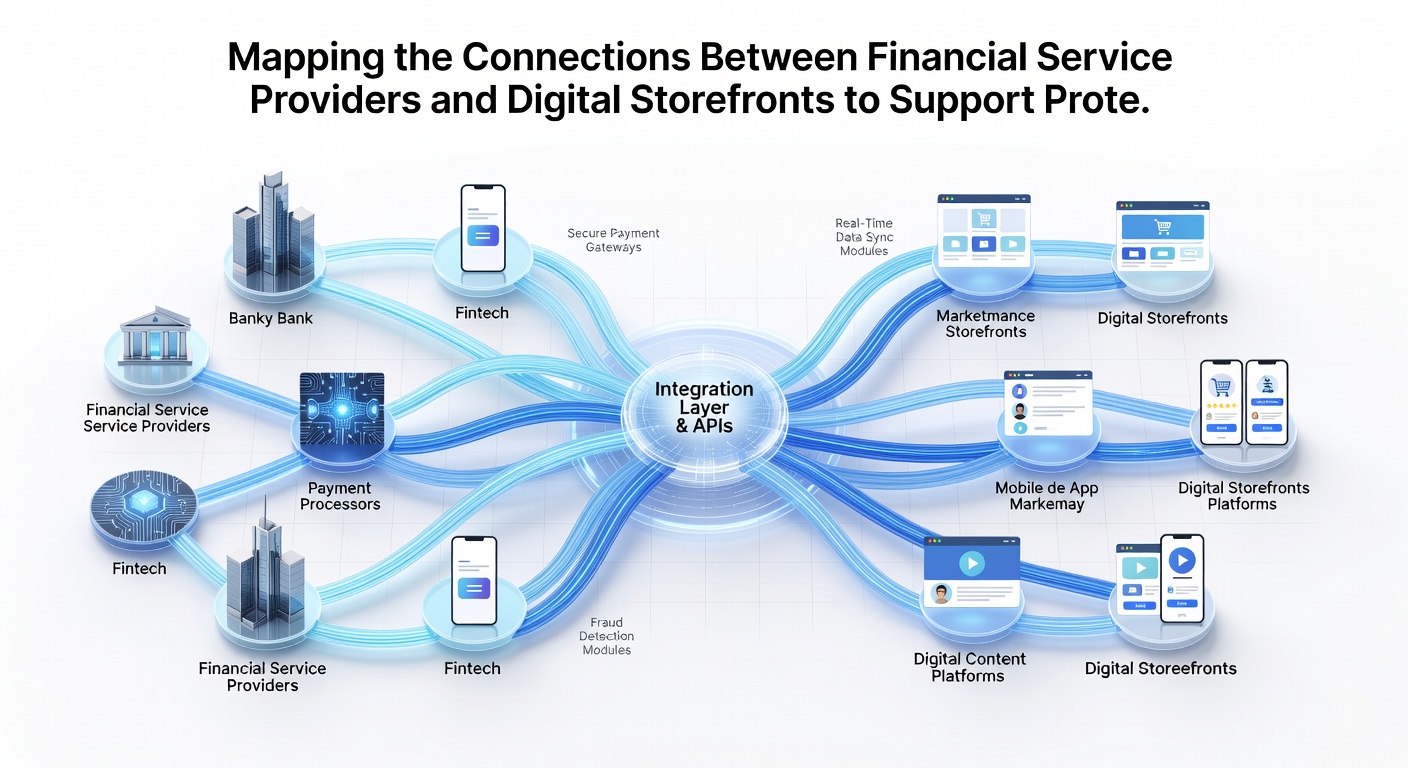

Financial service providers maintain direct linkages with digital storefronts through secure APIs and settlement networks that enable protected charge operations across retail platforms. These connections facilitate the flow of transaction data while incorporating verification protocols that align with banking standards established in multiple jurisdictions. Data from the Bank for International Settlements shows that integrated systems processed over 18 billion recurring and one-time charges in 2025 with layered security measures reducing unauthorized activity by measurable margins.

Protected charge operations rely on synchronized channels where banks and processors exchange authorization requests with storefront platforms in real time. Observers note that these mappings often include endpoint verification at both the merchant interface and the acquiring bank level which creates redundant checks before funds move. In June 2026 the Federal Reserve updated its payment system guidelines to emphasize standardized data fields for charge protection across digital channels and this adjustment prompted many providers to recalibrate their connection protocols accordingly.

Core Integration Points in Payment Ecosystems

Digital storefronts connect to financial institutions via gateway interfaces that route charge requests through encrypted tunnels and compliance layers. Researchers at the University of Toronto documented how these pathways incorporate account validation sequences that match customer details against issuer records before any deduction occurs. The process involves sequential handoffs between the storefront server, the payment processor, and the originating bank which together form a closed verification loop.

Mapping exercises reveal that protected operations depend on consistent identifier sharing across these nodes. Each participant in the chain receives tokenized or masked data sets that prevent exposure of full account details while still allowing the charge to clear. This structure supports both credit and debit flows and it scales to accommodate high-volume retail environments without introducing latency that disrupts customer checkout sequences.

Verification Layers and Data Exchange Protocols

Multiple verification stages operate in parallel once a charge request leaves the digital storefront. Banks apply risk scoring models that draw on historical transaction patterns and the storefront contributes session-level signals such as device fingerprints and IP geolocation. Together these elements produce a composite authorization decision that either approves or declines the protected charge within milliseconds.

Industry reports from the Australian Payments Network indicate that such layered exchanges lowered dispute rates in automated retail by 14 percent during the first half of 2026. The mappings also extend to post-authorization reconciliation where settlement files travel back through the same channels to confirm final posting and trigger any necessary adjustments.

Regulatory Alignment Across Regions

Financial service providers must satisfy overlapping requirements when linking to storefronts in different markets. European Central Bank standards for strong customer authentication influence how many US-based processors configure their API endpoints for cross-border charges. Canadian regulators through the Bank of Canada have similarly issued guidance on data residency that affects how transaction logs are stored and accessed during protected charge cycles.

These regional frameworks converge at the technical level through common message formats adn encryption requirements. Providers that map their connections comprehensively can therefore maintain compliance across borders while supporting storefronts that serve international customer bases. The result appears in unified dashboards that display authorization outcomes alongside regulatory status flags for each processed charge.

Scaling Protected Operations in High-Volume Retail

As digital storefronts expand their product catalogs and customer reach the underlying connections must handle increased charge volumes without compromising protection mechanisms. Load balancing across multiple processor endpoints and redundant banking channels becomes essential. Studies conducted by the Payments Research Institute found that retailers using diversified connection maps experienced 22 percent fewer interruptions during peak sales periods compared with single-channel setups.

Real-time monitoring tools sit atop these mappings and alert operators when latency or error rates exceed thresholds. Such visibility allows providers to reroute traffic dynamically while preserving the verification integrity that defines protected charge operations. The approach keeps systems resilient even when individual nodes encounter temporary outages or require maintenance.

Conclusion

Comprehensive mapping of connections between financial service providers and digital storefronts continues to underpin reliable protected charge operations. These architectures integrate verification protocols, settlement pathways, and regulatory controls into cohesive systems that process transactions securely. Ongoing refinements driven by updates such as those issued in June 2026 ensure the mappings remain aligned with evolving payment standards across major markets.