Mapping Verification Pathways in Automated Deduction Systems for Recurring US Retail Revenue Streams

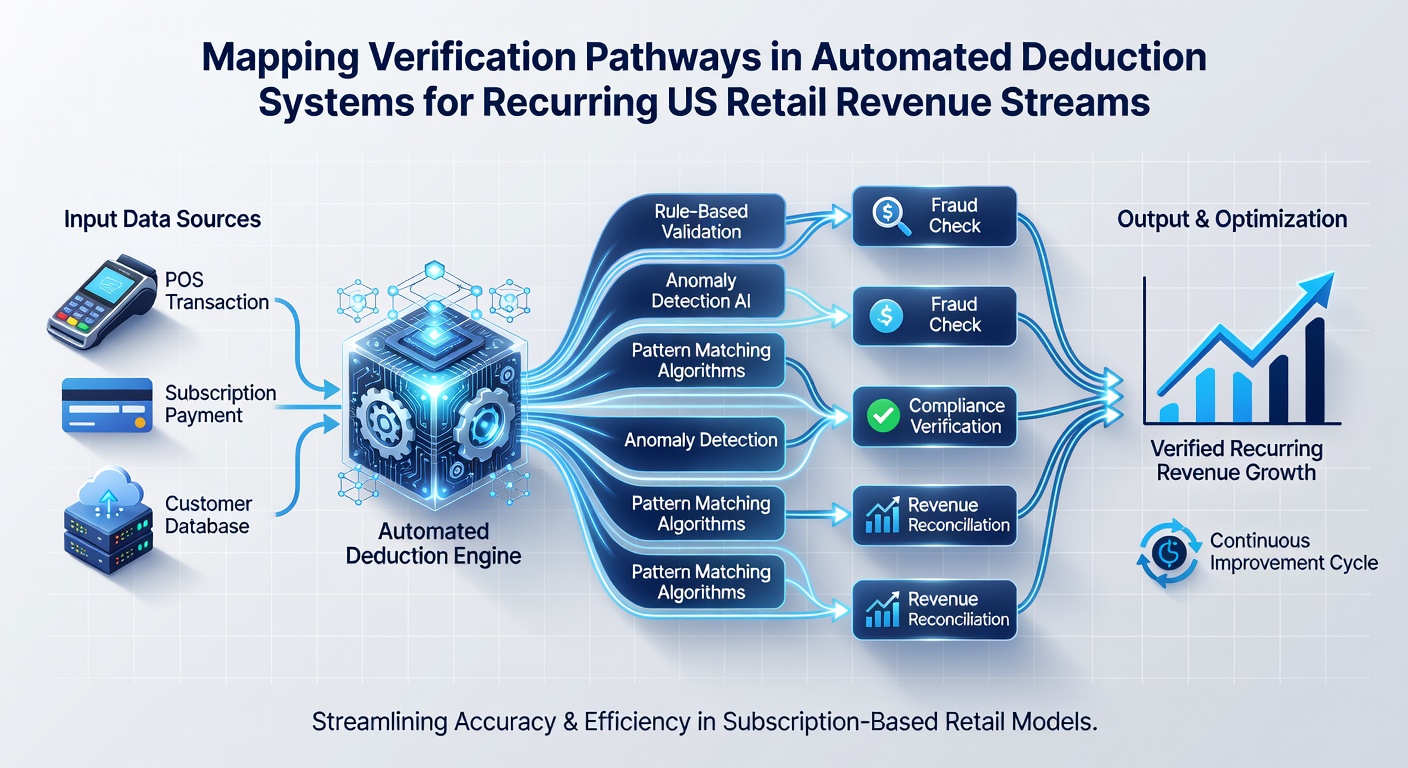

Retail operations across the United States rely on automated deduction systems to handle recurring revenue streams from subscriptions, memberships, and installment plans, where verification pathways serve as structured sequences that confirm transaction legitimacy before funds move. These pathways integrate multiple checkpoints including account validation, identity confirmation, and risk scoring modules that operate in sequence or parallel depending on system design. Data from the Federal Reserve indicates that recurring payment volumes in consumer retail reached significant levels by early 2025, with continued growth projected through 2026 as more merchants adopt subscription models.

Core Components of Verification Pathways

Automated deduction frameworks begin with initial account authentication that pulls data directly from banking networks or card issuers, then layer on behavioral analysis drawn from historical transaction patterns. Researchers at academic institutions have documented how these systems map decision trees that route each deduction request through specific verification nodes, such as address verification services or device fingerprinting tools. The process connects related checks with logical operators so that a failed step at one node triggers either escalation to manual review or outright rejection, while successful passages advance the request toward authorization.

Payment processors configure these pathways to accommodate both ACH transfers and credit card charges, ensuring that each route aligns with network rules set by operators like NACHA for electronic transactions. Observers note that mapping occurs during system implementation phases when developers define conditional branches based on factors including transaction amount thresholds, customer tenure metrics, and geographic indicators. This structured approach allows platforms to process high volumes without proportional increases in manual intervention.

Integration with Retail Revenue Cycles

US retail environments generate recurring streams through loyalty programs, software-as-a-service add-ons, and product replenishment services where deduction timing follows fixed schedules. Verification pathways synchronize with these cycles by embedding pre-authorization windows that run hours or days ahead of scheduled pulls, giving systems time to flag anomalies. Studies from industry research groups reveal that such pre-checks reduce processing failures by identifying issues like insufficient funds or closed accounts before they reach settlement stages.

Merchants integrate these mappings into enterprise resource planning tools so that revenue forecasts incorporate verified deduction success rates rather than raw billing attempts. In May 2026, updates to federal guidelines on consumer financial data access are expected to influence how verification layers pull real-time account status information, prompting retailers to adjust pathway configurations accordingly.

Technical Mapping Techniques

Developers employ flowchart representations and state machine models to visualize verification sequences, where each state represents a distinct check such as CVV validation for cards or routing number confirmation for bank accounts. These models connect states through transitions triggered by data inputs, allowing simulation of various scenarios before live deployment. Industry reports show that companies adopting formal mapping reduce integration errors during gateway connections by substantial margins compared with ad-hoc implementations.

Pathway adjustments occur when new fraud indicators emerge, such as unusual IP address clusters or mismatched billing details, prompting updates to decision rules within the automated framework. Those who maintain these systems often use version control practices to track changes across multiple retail client environments, ensuring consistency while permitting customization for specific revenue stream characteristics.

Regulatory Alignment and Data Handling

Verification pathways must comply with US regulations governing electronic payments and consumer data protection, including provisions that require clear disclosure of deduction terms at enrollment. Systems incorporate consent verification steps that log customer agreements alongside transaction records, creating audit trails that support regulatory examinations. Data indicates that platforms maintaining comprehensive logs experience fewer compliance issues during periodic reviews by oversight bodies.

Cross-border elements appear when US retailers serve international customers, requiring pathways to incorporate additional checks aligned with frameworks from regions like the European Union or Canada. These adaptations maintain core US requirements while adding jurisdiction-specific nodes for currency conversion validation or tax identification confirmation.

Performance Monitoring and Refinement

Retail operators track key metrics such as approval rates, retry success percentages, and false positive rejection figures to evaluate pathway effectiveness over time. Continuous monitoring feeds into refinement cycles where analysts identify bottlenecks in verification sequences and redistribute check priorities accordingly. Evidence from payment industry analyses demonstrates that iterative mapping updates correlate with improved retention in recurring billing programs.

Collaboration between merchants and technology providers facilitates these refinements through shared data exchanges that highlight emerging patterns in deduction outcomes. Such partnerships enable rapid incorporation of new verification methods as they become available from network operators or third-party service vendors.

Conclusion

Mapping verification pathways within automated deduction systems provides US retail businesses with structured methods to manage recurring revenue streams securely and efficiently. The combination of sequential checks, regulatory alignment, and ongoing performance tracking supports stable operations across diverse subscription models. As payment networks evolve and new data access standards take effect in 2026, these mapped systems continue to adapt while preserving core verification integrity.