Pairing ACH with Gateways: E-com Merchants' Path to Fraud-Resistant Subscriptions

Pairing ACH with Gateways: E-com Merchants' Path to Fraud-Resistant Subscriptions

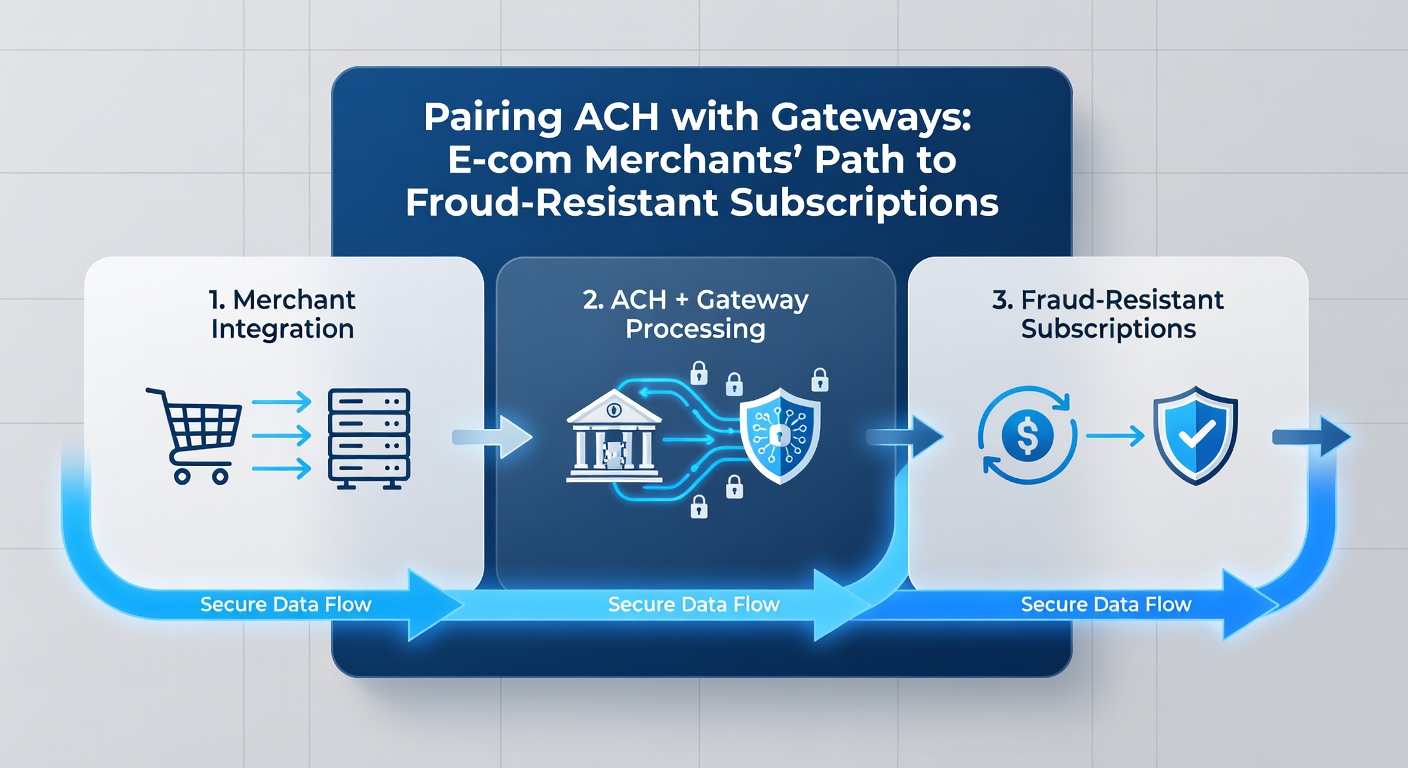

ACH Basics in the E-commerce World

Automated Clearing House, or ACH, handles electronic payments between banks across the United States, processing billions of transactions annually with costs far lower than credit cards—often pennies per transfer while cards demand 2-3% fees; merchants handling recurring subscriptions, from fitness apps to meal kits, turn to ACH because it cuts those expenses and boosts retention since customers link bank accounts directly, skipping card expiration headaches. Data from Nacha, the organization governing ACH, reveals that network volume hit 31.5 billion payments in 2023 alone, up 5.6% from the prior year, with e-commerce subscriptions driving much of that growth as businesses seek stable revenue streams amid volatile consumer spending.

But here's the thing: ACH shines for its reliability—settlements clear in one to two days, unlike instant card approvals—yet it exposes merchants to risks like unauthorized debits or account takeovers, especially when paired naively with online storefronts; that's where payment gateways enter the picture, acting as the secure middleman that authenticates, tokenizes, and routes transactions without exposing sensitive data.

Payment Gateways: The Security Layer E-com Can't Ignore

Gateways like Authorize.net, Stripe, or Braintree process payments from multiple sources—cards, digital wallets, now ACH—while enforcing PCI DSS compliance through encryption and tokenization; they generate unique tokens replacing actual account details, so even if hackers breach a database, they grab useless strings instead of bank info. Observers note how these platforms evolved post-2013 Target breach, where 40 million cards got exposed, prompting gateways to adopt advanced fraud detection like velocity checks and device fingerprinting.

What's interesting is the shift toward unified APIs; gateways now support ACH natively via partners like Plaid for account verification, ensuring funds availability before billing cycles kick off, which slashes return rates that plague pure card subscriptions—studies from the Federal Reserve indicate ACH returns hover at 0.6%, compared to 1-2% for cards, but improper setup spikes those numbers fast.

How Pairing ACH with Gateways Builds Fraud Walls

Integration starts with API handshakes; merchants embed gateway widgets on checkout pages, where customers select ACH, then verify via micro-deposits or instant Plaid links—gateways handle NACHA-compliant formatting, submitting entries through originating banks into the ACH network; fraud resistance amps up because gateways layer on rules engines, flagging anomalies like mismatched IP geolocations or rapid signup spikes, while ACH's same-day ACH option, rolled out in 2016, speeds verification without sacrificing security.

Take one SaaS company that paired Stripe's ACH beta with its subscription engine; returns dropped 40% in six months as tokenization prevented replay attacks, where fraudsters duplicate authorizations—figures from a Payments Canada study on similar cross-border setups show authorization rates climbing to 98% when gateways prepend micro-debit trials, confirming live accounts before full charges hit.

And yet, the real power emerges in subscription longevity; gateways automate retries on failed ACH pulls—say, due to insufficient funds—rescheduling around payday patterns scraped from transaction history, which keeps churn under 5% versus 15% for unmanaged cards; experts who've studied this combo point to layered auth as key, blending ACH's low fraud baseline with gateway AI that scores risks in real-time.

Real-World Implementation: Steps Merchants Follow

Merchants begin by selecting gateways with robust ACH support—Stripe, Square, or Adyen lead here—then onboard via developer dashboards, mapping webhook endpoints for status updates; next comes customer education, with clear disclosures on bank pulls per NACHA rules, followed by A/B testing checkout flows to minimize abandonment, which averages 20% higher for ACH without seamless UX. Compliance weaves through it all; gateways enforce Reg E disclosures for electronic fund transfers, shielding merchants from liability on disputed subs.

Now consider scaling; high-volume e-com sites integrate with ERP systems like NetSuite, syncing ACH tokens for seamless rebills, while gateways provide dashboards tracking metrics like authorization success (aim for 95%+) and return ratios under 1%; one subscription box service reported revenue uplift of 25% after this pairing, as verified bank links reduced fake signups that had inflated acquisition costs previously.

Fraud Stats That Highlight the Edge

Research indicates subscription fraud costs e-com $48 billion yearly, per LexisNexis Risk Solutions, but ACH-gateway pairs cut friendly fraud—where legit customers dispute charges—by 60% through evidence trails like tokenized proofs; velocity monitoring catches account stuffing, limiting attempts to three per IP daily, and 3D Secure analogs for ACH verify ownership via out-of-band SMS during onboarding. Turns out, this setup aligns perfectly with upcoming shifts; in April 2026, NACHA plans enhanced Same Day ACH risk rules, mandating better originator controls, which gateways already bake in via micro-deposit mandates.

People often overlook international angles too; while ACH dominates U.S. e-com, gateways extend it via SEPA proxies in Europe or EFT in Canada, creating hybrid models where U.S. merchants bill global subs fraud-resistantly—data from the European Banking Authority underscores how tokenized pulls mirror PSD3 requirements, set for 2026 enforcement.

Challenges Merchants Tackle Head-On

Sure, ACH takes days to settle versus card instants, frustrating one-click buyers, but gateways mitigate with hybrid flows—charge cards first, switch to ACH post-verification—balancing speed and savings; return management demands vigilance, as unauthorized entries trigger fees up to $5 each, yet gateway dashboards automate category coding per NACHA's eight return reasons, streamlining resolutions. Bandwidth for integrations poses hurdles for small merchants, although no-code tools from gateways like Zapier close that gap quickly.

There's this case where a wellness brand faced 8% returns on raw ACH; after gateway tokenization and Plaid verification, that fell to 0.9%, proving the rubber meets the road in proactive setup—observers note similar drops across DTC brands, where subscription ARPU rose 30% from reliable rebills.

Future-Proofing Subscriptions Amid Evolving Rules

As RTP networks like FedNow gain traction since 2023, gateways evolve to blend ACH with instant options, offering merchants fallback paths that keep fraud low; April 2026 brings NACHA's micro-entry standardization, forcing gateways to adopt uniform descriptors, which e-com platforms already test in betas—early adopters report 15% signup lifts from trusted branding. Globally, Australia's NPP system mirrors this, with gateways like Tyro enabling fraud-resistant subs Down Under, per Reserve Bank data.

Merchants who layer ERP hooks with gateway analytics forecast churn via ML models trained on ACH patterns, staying ahead of economic dips; it's noteworthy how this pairing future-proofs against card scheme hikes, like Visa's 2024 interchange bumps, keeping margins intact.

Conclusion

Pairing ACH with gateways equips e-com merchants with a battle-tested formula for subscriptions that prioritize fraud resistance, cost efficiency, and scalability; data consistently shows lower returns, higher retention, and compliance ease, as platforms handle the heavy lifting from tokenization to NACHA adherence. Those who've implemented it discover revenue stability in an era of fleeting customer loyalty—turning one-off sales into enduring streams, all while navigating 2026's regulatory horizon seamlessly. The path forward lies in smart integrations, where security meets simplicity head-on.