Regulatory Frameworks Guiding Secure Transaction Flows in Subscription Services for United States E-Commerce Operators

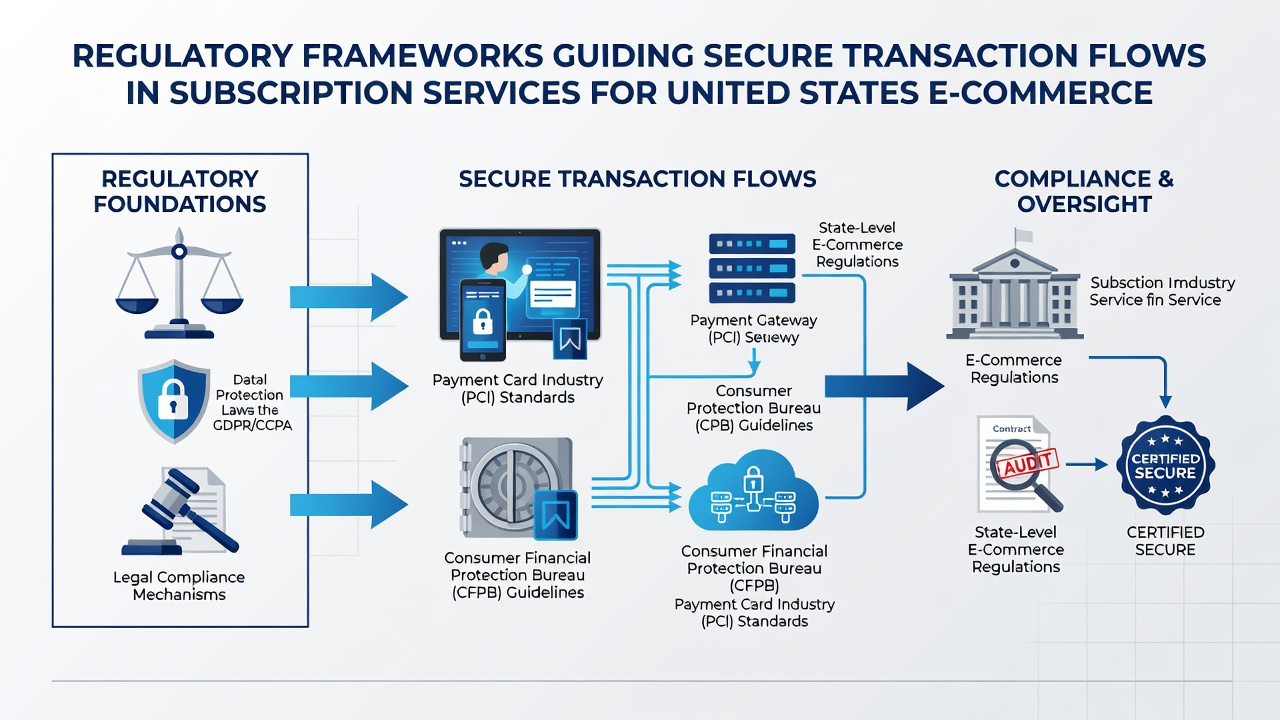

United States e-commerce operators handling subscription services navigate a layered system of federal statutes along with state-level requirements that shape how recurring payments move through secure channels. These frameworks address consumer protections, data security standards, and electronic fund transfer rules while operators manage automated billing cycles that depend on consistent authorization and verification processes.

The Electronic Fund Transfer Act combined with its implementing Regulation E establishes baseline protections for consumers who authorize recurring debits from bank accounts, requiring clear disclosure of terms and procedures for stopping payments or resolving errors. Operators must maintain records of authorizations that demonstrate affirmative consent rather than assumed renewals, and this documentation supports audit trails that financial institutions review during transaction settlement.

Federal Consumer Protection Standards for Recurring Billing

The Federal Trade Commission enforces rules around negative option marketing that directly affect subscription models, where consumers receive goods or services on an ongoing basis unless they take affirmative steps to cancel. Amendments effective in prior years strengthened requirements for clear and conspicuous disclosures at multiple points in the customer journey, including initial sign-up and renewal notices, while operators document how these disclosures appear in digital interfaces.

Research from regulatory filings indicates that enforcement actions have targeted platforms failing to provide easy cancellation mechanisms, prompting many e-commerce operators to integrate standardized consent flows that record timestamps and IP addresses alongside customer acknowledgments. These records become essential when disputes arise over whether a transaction truly reflected ongoing authorization.

Payment Card Industry Standards and Data Security Integration

Although PCI DSS operates as an industry standard rather than a statute, federal agencies reference compliance expectations when examining data breaches involving stored card credentials used for subscriptions. Operators segment cardholder data environments and employ encryption protocols that align with both security requirements and emerging state privacy statutes such as those modeled after teh California Consumer Privacy Act framework.

State attorneys general have coordinated enforcement around data minimization principles, requiring operators to retain only the information necessary for transaction processing and dispute resolution rather than indefinite storage of full account details. In June 2026 several multistate settlements highlighted platforms that retained legacy card data beyond required retention periods, resulting in mandated audits and enhanced logging procedures that now serve as reference points for similar operators.

State-Level Auto-Renewal and Notice Requirements

Multiple states maintain specific statutes governing automatic renewals that supplement federal rules, with notice periods ranging from 30 to 60 days before renewal dates depending on subscription length. Operators serving national audiences implement centralized systems capable of generating jurisdiction-specific disclosures that reference applicable state codes while maintaining uniform backend authorization logic across payment rails.

Observers tracking enforcement patterns note that states like New York and Florida have updated their requirements to include email and in-app notifications that must contain direct links to cancellation portals, reducing friction that previously led to complaints filed with consumer protection agencies. These layered obligations encourage operators to maintain compliance matrices that map each customer’s billing address to the relevant state mandates.

Emerging Coordination Between Federal Agencies

The Consumer Financial Protection Bureau continues to examine how electronic payment authorizations intersect with fair lending considerations, particularly when subscription models incorporate dynamic pricing or promotional trial periods that convert to paid recurring charges. Guidance issued in recent years encourages operators to test disclosure language for clarity across diverse consumer populations and to retain evidence of such testing.

International frameworks such as those administered by the Federal Trade Commission provide comparative reference points, while Canadian regulatory approaches to recurring payments offer additional models that some US-based platforms study when designing cross-border subscription flows. Academic analyses from institutions including the University of Michigan’s Ross School of Business have examined how these overlapping requirements influence platform architecture decisions around authentication timing and retry logic for failed transactions.

Conclusion

Operators in the United States subscription e-commerce space align operational practices with an interconnected set of federal statutes, state auto-renewal laws, and security standards that collectively govern authorization, disclosure, and data handling. Continued coordination among agencies, combined with enforcement actions that reference specific technical controls, shapes how platforms structure recurring transaction pathways while maintaining compliance across jurisdictions.