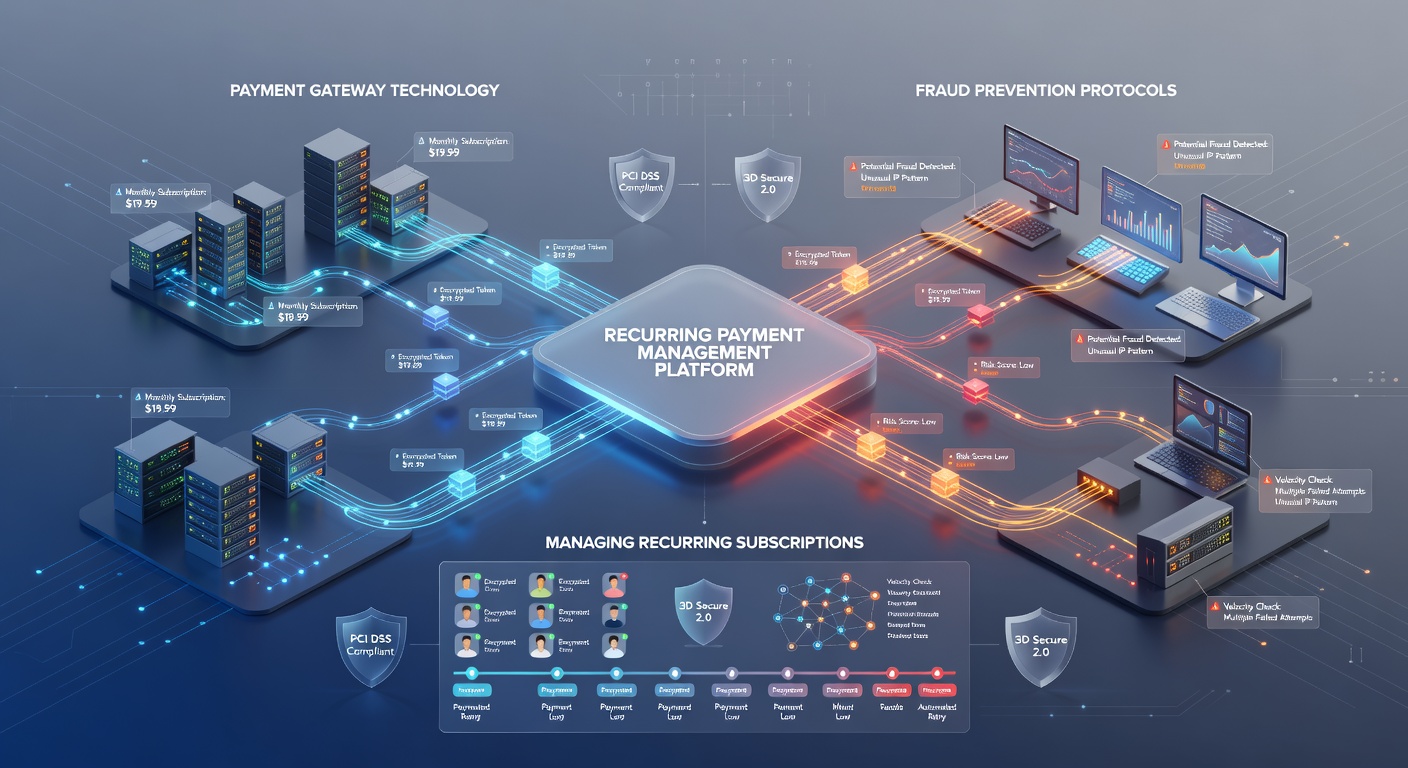

The Intersection of Payment Gateway Technology and Fraud Prevention Protocols in Managing Recurring Customer Payments

Payment gateways serve as the technical backbone that processes recurring customer payments while embedding fraud prevention protocols directly into their transaction flows, and this integration has grown more layered as subscription models expanded across industries since the mid-2010s. Observers note that gateways now routinely apply layered checks such as address verification systems, card verification values, and device fingerprinting at the moment a recurring authorization request arrives, which reduces the window for unauthorized activity before funds move. Data from payment processors shows that these combined measures handle millions of subscription renewals daily, with velocity monitoring tools tracking patterns like rapid successive attempts from single IP addresses or mismatched billing details across multiple cycles. Experts have observed that machine learning models within modern gateways analyze historical transaction data to flag anomalies specific to recurring setups, such as sudden changes in payment amounts or billing frequencies that deviate from established customer profiles. These systems update continuously because subscription services generate predictable yet high-volume traffic that fraudsters target through stolen credentials or account takeover attempts. Research indicates that gateways incorporating behavioral biometrics, including keystroke patterns and mouse movements during checkout flows, achieve measurable reductions in chargeback rates for recurring merchants compared with static rule-based approaches alone.

Payment gateways serve as the technical backbone that processes recurring customer payments while embedding fraud prevention protocols directly into their transaction flows, and this integration has grown more layered as subscription models expanded across industries since the mid-2010s. Observers note that gateways now routinely apply layered checks such as address verification systems, card verification values, and device fingerprinting at the moment a recurring authorization request arrives, which reduces the window for unauthorized activity before funds move. Data from payment processors shows that these combined measures handle millions of subscription renewals daily, with velocity monitoring tools tracking patterns like rapid successive attempts from single IP addresses or mismatched billing details across multiple cycles. Experts have observed that machine learning models within modern gateways analyze historical transaction data to flag anomalies specific to recurring setups, such as sudden changes in payment amounts or billing frequencies that deviate from established customer profiles. These systems update continuously because subscription services generate predictable yet high-volume traffic that fraudsters target through stolen credentials or account takeover attempts. Research indicates that gateways incorporating behavioral biometrics, including keystroke patterns and mouse movements during checkout flows, achieve measurable reductions in chargeback rates for recurring merchants compared with static rule-based approaches alone.Core Technologies Enabling Secure Recurring Processing

Tokenization replaces sensitive card data with unique identifiers that gateways store and reuse for subsequent billing cycles, which limits exposure if a merchant database faces compromise. Payment service providers report that tokenized recurring transactions experience lower fraud incidence because the actual card details never touch the merchant environment after initial setup. Those who've studied gateway architectures point out that this approach pairs naturally with automated credential-on-file protocols that require periodic re-authentication triggers when risk scores rise.

Three-domain secure protocols have extended their reach into recurring scenarios through exemptions and delegated authentication models that gateways manage on behalf of issuers. In practice, a gateway might apply strong customer authentication only on the first payment while using risk-based rules for later cycles, and this balance keeps friction low for legitimate subscribers. Figures from the European Central Bank highlight steady adoption of these dynamic authentication frameworks across the region as merchants seek compliance with evolving security standards.

Protocol Layers That Address Subscription-Specific Risks

Fraud prevention in recurring payments often relies on account updater services that gateways integrate to refresh expired card details automatically, which prevents legitimate declines from escalating into lost revenue or customer complaints. Researchers discovered that combining these services with real-time screening for known compromised credentials creates a tighter net around recurring flows without interrupting service continuity. Observers note that gateways also deploy geo-location checks and proxy detection to spot when a renewal request originates from unexpected regions relative to the customer's historical activity.

By May 2026 several gateway providers plan to roll out enhanced consortium-based data sharing networks that allow real-time exchange of fraud signals across different payment rails while preserving privacy controls. This development builds on existing collaborative databases that already help identify patterns such as BIN attacks targeting subscription services. Industry reports reveal that merchants using these shared intelligence layers see faster identification of emerging threats compared with isolated monitoring setups.

Regulatory and Operational Considerations in 2026

Compliance frameworks continue to shape how gateways implement fraud controls for recurring billing, with requirements around data retention and customer notification influencing protocol design choices. Those monitoring regulatory updates across North America and Europe describe a trend toward mandating periodic risk assessments for high-volume subscription processors. Gateways respond by embedding audit trails that capture every authentication decision, making it easier for merchants to demonstrate adherence during reviews.

Operational teams at payment providers often test protocol effectiveness through controlled simulations that mimic common recurring fraud vectors like card testing or friendly fraud claims. These exercises generate datasets that refine detection thresholds over time, and the resulting adjustments help maintain approval rates while containing losses. Evidence suggests that gateways balancing automated rules with human oversight teams achieve more stable performance across seasonal subscription peaks.

Conclusion

The ongoing evolution of payment gateway technology demonstrates clear technical synergy with fraud prevention protocols when managing recurring customer payments, as evidenced by widespread deployment of tokenization, adaptive authentication, and collaborative monitoring tools. Available data through 2026 continues to track improvements in transaction security metrics for subscription-based merchants who adopt these integrated approaches. Future refinements will likely center on tighter interoperability between gateways and emerging verification standards across global markets.