Tracing Digital Exchange Networks: Aligning Verification Layers With Banking Channels in Automated Retail Ecosystems

Automated retail ecosystems rely on intricate digital exchange networks that track transactions from shelf to settlement, and alignment between verification layers and banking channels forms the backbone of these operations. Systems in large-scale automated stores process thousands of exchanges daily while pulling data from inventory sensors, customer interfaces, and payment rails to maintain accurate records. Observers note that this tracing capability has expanded steadily since the early 2020s as retailers adopted real-time data flows to reduce discrepancies between physical goods movement and financial reconciliation.

Core Components of Digital Exchange Networks

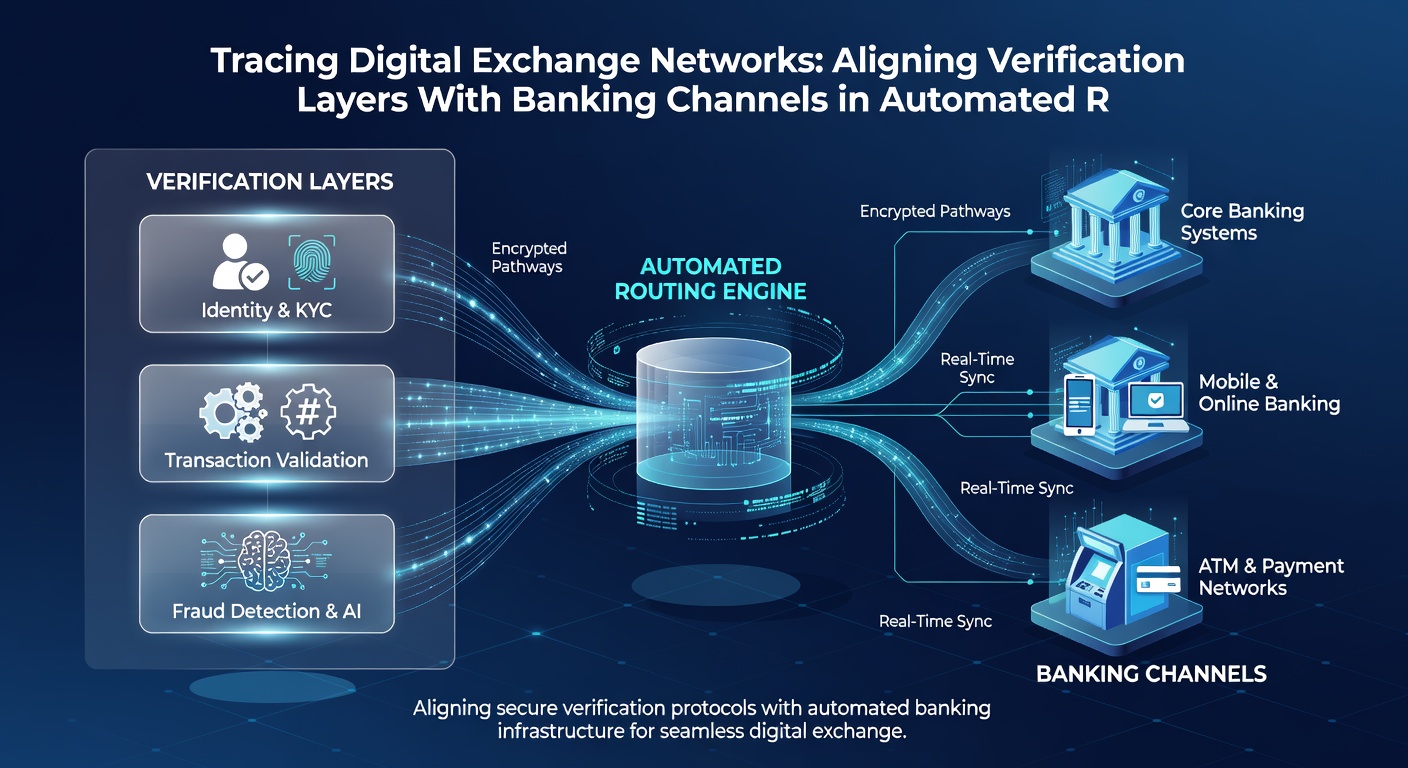

Digital exchange networks consist of interconnected nodes that capture item-level data, customer identifiers, and transaction timestamps before routing that information through verification checkpoints. Retail operators integrate radio-frequency identification tags with point-of-sale terminals and cloud-based ledgers so each exchange carries a traceable identifier from the moment a product leaves the shelf. Data shows these networks handle both high-volume small transactions and occasional larger orders while maintaining audit trails that banks later reference during reconciliation cycles.

Verification layers sit between the retail environment and banking infrastructure to confirm identity, authorization, and fund availability without introducing noticeable delays at checkout. These layers pull from multiple data sources including government-issued identification databases, credit bureaus, and internal risk models before passing a verified signal to the banking channel. Researchers discovered that synchronization between these layers and banking protocols reduces settlement failures by matching transaction attributes such as amount, timestamp, and merchant category code in a single pass.

Banking Channel Integration Points

Banking channels accept verified payloads from retail networks through standardized messaging formats that comply with ISO 20022 guidelines adopted across North America and parts of Asia. Automated retail platforms format exchange data to include verification results so receiving banks can apply their own fraud filters and liquidity checks without requesting additional customer details. The European Central Bank published updates in 2025 that encouraged similar formatting for cross-border retail flows, and those changes took full effect by early 2026.

Real-time alignment requires application programming interfaces that connect retail verification engines directly to banking authorization endpoints. When a customer completes a purchase in an automated store, the verification layer transmits a tokenized identifier along with the transaction amount to the bank, which then confirms available funds and posts a provisional hold. This process completes in under two seconds in most documented deployments, allowing the system to release goods or trigger restocking alerts simultaneously.

Tracing Mechanisms and Data Standards

Tracing occurs through immutable logs that record every handoff between verification layers and banking channels, creating an end-to-end view of each exchange. Retail systems timestamp these logs at the point of capture, verification approval, bank authorization, and final settlement so discrepancies surface quickly during daily batch reviews. Studies from university research groups indicate that stores using unified logging reduced reconciliation time by an average of 40 percent compared with fragmented record-keeping approaches.

Standards bodies continue refining data fields that support this tracing while preserving privacy requirements. In May 2026 several North American processors began testing an expanded set of metadata fields that include product category verification codes alongside banking authorization responses. Early results from pilot programs show these fields allow banks to apply more granular compliance checks without increasing average processing latency.

Operational Patterns Across Retail Segments

Grocery and convenience operators lead adoption of aligned verification and banking setups because their high transaction counts expose gaps in legacy reconciliation methods. Distribution centers feeding automated stores feed inventory data into the same networks so verification layers can cross-check stock levels against pending customer orders before funds move. This closed loop prevents over-authorization when popular items run low during peak hours.

Observers note that department store chains and specialty retailers follow similar patterns but often layer additional verification for higher-value items. These operators route exchanges through the same banking channels yet insert extra identity checks that still conform to the shared messaging standards. The result is a scalable framework that accommodates both rapid small purchases and slower, higher-scrutiny transactions within one infrastructure.

Conclusion

Tracing digital exchange networks while aligning verification layers with banking channels continues to shape how automated retail ecosystems process transactions at scale. Standardized messaging, real-time interfaces, and unified logging provide the technical foundation that supports both operational efficiency and regulatory compliance. As processors roll out expanded metadata fields in 2026, the same alignment principles extend to new retail formats and geographic markets without requiring separate verification stacks for each banking partner.